Download IRS Schedule C 1040 Template

Misconceptions

The IRS Schedule C (Form 1040) is an important document for self-employed individuals and sole proprietors. However, several misconceptions surround this form, which can lead to confusion and potential errors in tax reporting. Here are seven common misconceptions about Schedule C:

- Only businesses with large revenues need to file Schedule C. Many believe that Schedule C is only for high-earning businesses. In reality, any self-employed individual or sole proprietor, regardless of income level, must report their earnings using this form.

- Expenses can only be deducted if they are directly related to the business. While it's true that business expenses must be necessary and ordinary, some may not realize that expenses related to the home office, vehicle use, and even certain meals can also be deducted if they meet IRS criteria.

- All income must be reported on Schedule C, even if it’s not received in cash. Some individuals think they can ignore income not received in cash. However, the IRS requires that all income, including bartering and non-cash transactions, be reported on Schedule C.

- Filing Schedule C guarantees a higher chance of an audit. There is a perception that filing Schedule C increases the likelihood of being audited. While self-employed individuals may face more scrutiny, audits are based on various factors, not solely on the form itself.

- Once filed, Schedule C cannot be amended. Some people believe that once they submit Schedule C, they cannot make changes. In fact, taxpayers can amend their returns using Form 1040-X if they discover errors or need to adjust their reported income or expenses.

- All self-employed individuals need to file Schedule C. Not every self-employed person must file this form. For example, those earning less than $400 in net income from self-employment may not need to file Schedule C, but they should still report any income on their tax return.

- Filing Schedule C is the same as filing a business tax return. Many mistakenly think that Schedule C is a complete business tax return. While it does report business income and expenses, it is part of the individual tax return (Form 1040) and does not replace the need for other business filings, if applicable.

Understanding these misconceptions can help individuals navigate the complexities of self-employment taxation more effectively. Accurate reporting on Schedule C is crucial for compliance and can ultimately impact financial outcomes.

File Details

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule C (Form 1040) is used by sole proprietors to report income and expenses from their business. |

| Eligibility | Any individual who operates a business as a sole proprietor can file this form, regardless of the business's size or income level. |

| Filing Deadline | Schedule C must be filed by the tax deadline, which is typically April 15th, unless an extension is requested. |

| Net Profit or Loss | At the end of the form, you will calculate your net profit or loss, which is crucial for determining your taxable income. |

| Expenses | Common business expenses can be deducted, including rent, utilities, and supplies, reducing your taxable income. |

| Record Keeping | It's essential to maintain accurate records of all income and expenses to support the information reported on Schedule C. |

| Self-Employment Tax | Income reported on Schedule C may be subject to self-employment tax, which covers Social Security and Medicare contributions. |

| State-Specific Forms | Some states require additional forms for reporting business income; check your state’s tax regulations for specifics. |

| Form Updates | The IRS updates Schedule C periodically, so it's important to use the latest version when filing your taxes. |

| Consulting a Professional | If you're unsure about how to fill out Schedule C, consider consulting a tax professional for guidance. |

Key takeaways

Schedule C is used by sole proprietors to report income and expenses from their business activities. This form is essential for individuals operating as self-employed, freelancers, or independent contractors.

Accurate record-keeping is crucial. Gather all relevant financial documents, including invoices, receipts, and bank statements, to ensure that income and expenses are reported correctly.

Clearly distinguish between personal and business expenses. Only business-related expenses are deductible, so maintaining separate accounts can simplify this process.

Expenses can include a variety of costs such as rent, utilities, supplies, and travel. Familiarize yourself with which expenses are allowable to maximize your deductions.

Net profit or loss from Schedule C will affect your overall tax liability. This figure is transferred to your Form 1040, impacting your taxable income.

Self-employment tax applies to net earnings from self-employment. Be prepared to calculate this tax, as it is separate from income tax.

Filing deadlines are important. Schedule C must be submitted by the same deadline as your personal income tax return, typically April 15.

Consider consulting a tax professional if your situation is complex. They can provide guidance on maximizing deductions and ensuring compliance with tax laws.

Dos and Don'ts

When completing the IRS Schedule C (Form 1040), which is essential for reporting income or loss from a business you operated or a profession you practiced as a sole proprietor, there are several key actions to consider. Here are four important dos and don’ts to keep in mind:

- Do ensure that all income is accurately reported. This includes cash, checks, and any other forms of payment received for your services or products.

- Do keep thorough records of all business expenses. Receipts and documentation can help substantiate your claims and ensure compliance.

- Don't overlook the importance of categorizing your expenses correctly. Misclassifying expenses can lead to errors that might raise red flags with the IRS.

- Don't forget to sign and date the form before submitting it. An unsigned form is considered incomplete and may delay processing.

Common mistakes

-

Incorrect Business Name: Many people forget to write their business name exactly as it appears on their official documents. This can lead to confusion and delays.

-

Missing Employer Identification Number (EIN): If your business requires an EIN, failing to include it can cause issues. Always check if you need one and provide it if necessary.

-

Incorrect Income Reporting: Some individuals report gross receipts inaccurately. It’s crucial to ensure that the figures reflect actual income earned during the year.

-

Overlooking Business Expenses: Many forget to claim all eligible business expenses. This can include costs for supplies, travel, and home office deductions. Review your expenses thoroughly.

-

Neglecting to Separate Personal and Business Expenses: Mixing personal and business expenses can lead to significant errors. Always maintain clear records to avoid this mistake.

-

Improper Use of Accounting Methods: Choosing the wrong accounting method, whether cash or accrual, can impact your reported income. Be sure to select the method that accurately reflects your business operations.

-

Not Keeping Adequate Records: Failing to maintain proper documentation can lead to discrepancies. Keep receipts and records organized to support your reported figures.

-

Missing Signature: It’s easy to forget to sign the form. A missing signature can delay processing and create unnecessary complications.

-

Not Seeking Professional Help: Some individuals attempt to fill out the form without seeking advice. Consulting a tax professional can help avoid common pitfalls and ensure accuracy.

What You Should Know About This Form

-

What is IRS Schedule C?

IRS Schedule C is a form used by sole proprietors to report income and expenses from their business. It is filed as part of the individual income tax return, Form 1040. This form helps the IRS determine the net profit or loss of your business, which is then included in your overall taxable income.

-

Who needs to file Schedule C?

If you operate a business as a sole proprietor, you are required to file Schedule C. This includes freelancers, independent contractors, and anyone who earns income from self-employment. If your business is structured as a partnership, corporation, or LLC, you would use different forms.

-

What types of income should be reported on Schedule C?

All income generated from your business activities should be reported. This includes sales revenue, commissions, fees, and any other income received for services rendered. It's important to keep accurate records of all income sources to ensure compliance and accuracy when filing.

-

What expenses can be deducted on Schedule C?

Many business-related expenses can be deducted, reducing your taxable income. Common deductions include:

- Cost of goods sold

- Advertising and marketing costs

- Rent or lease payments for business property

- Utilities, such as electricity and internet

- Business insurance

- Professional fees, such as legal and accounting services

It's crucial to maintain receipts and documentation for all expenses claimed to substantiate your deductions.

-

When is Schedule C due?

Schedule C is due on the same date as your personal income tax return, typically April 15th. If you need more time, you can file for an extension, which usually gives you until October 15th to submit your return. However, any taxes owed must still be paid by the original due date to avoid penalties and interest.

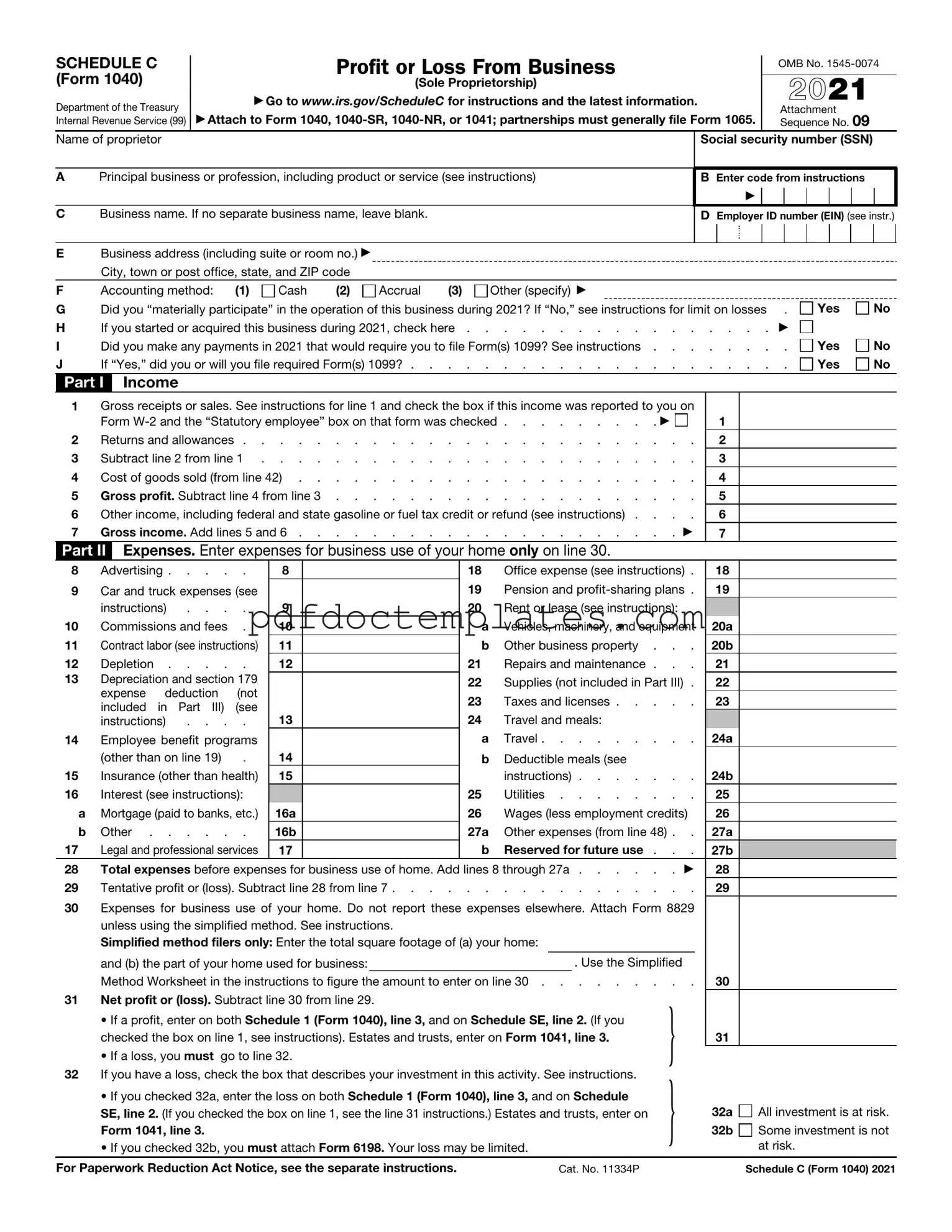

IRS Schedule C 1040 Example

SCHEDULE C (Form 1040)

Department of the Treasury Internal Revenue Service (99)

Profit or Loss From Business

(Sole Proprietorship)

▶Go to www.irs.gov/ScheduleC for instructions and the latest information.

▶Attach to Form 1040,

OMB No.

2021

Attachment Sequence No. 09

Name of proprietor

APrincipal business or profession, including product or service (see instructions)

CBusiness name. If no separate business name, leave blank.

Social security number (SSN)

BEnter code from instructions

▶

DEmployer ID number (EIN) (see instr.)

EBusiness address (including suite or room no.) ▶

City, town or post office, state, and ZIP code

F |

Accounting method: |

(1) |

Cash |

(2) |

|

Accrual |

(3) |

Other (specify) ▶ |

|

|

|

|

|

|

|

||||||

G |

Did you “materially participate” in the operation of this business during 2021? If “No,” see instructions for limit on losses |

. |

Yes |

No |

|||||||||||||||||

H |

If you started or acquired this business during 2021, check here |

. . |

. . |

▶ |

|

|

|||||||||||||||

I |

Did you make any payments in 2021 that would require you to file Form(s) 1099? See instructions . . . |

. . |

. . |

. |

Yes |

No |

|||||||||||||||

J |

If “Yes,” did you or will you file required Form(s) 1099? |

. . |

. . |

. |

Yes |

No |

|||||||||||||||

Part I |

Income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Gross receipts or sales. See instructions for line 1 and check the box if this income was reported to you on |

|

|

|

|

|

|||||||||||||||

|

Form |

. . . . . . . . . ▶ |

1 |

|

|

|

|

||||||||||||||

2 |

Returns and allowances |

2 |

|

|

|

|

|||||||||||||||

3 |

Subtract line 2 from line 1 |

3 |

|

|

|

|

|||||||||||||||

4 |

Cost of goods sold (from line 42) |

4 |

|

|

|

|

|||||||||||||||

5 |

Gross profit. Subtract line 4 from line 3 |

5 |

|

|

|

|

|||||||||||||||

6 |

Other income, including federal and state gasoline or fuel tax credit or refund (see instructions) . . . . |

6 |

|

|

|

|

|||||||||||||||

7 |

Gross income. Add lines 5 and 6 |

. . . . . . . . . |

. ▶ |

7 |

|

|

|

|

|||||||||||||

Part II |

Expenses. Enter expenses for business use of your home only on line 30. |

|

|

|

|

|

|

|

|||||||||||||

8 |

Advertising |

8 |

|

|

|

|

|

|

18 |

Office expense (see instructions) . |

18 |

|

|

|

|

||||||

9 |

Car and truck expenses (see |

|

|

|

|

|

|

|

19 |

Pension and |

19 |

|

|

|

|

||||||

|

instructions) . . . . |

9 |

|

|

|

|

|

|

20 |

Rent or lease (see instructions): |

|

|

|

|

|

||||||

10 |

Commissions and fees . |

10 |

|

|

|

|

|

|

a |

Vehicles, machinery, and equipment |

20a |

|

|

|

|

||||||

11 |

Contract labor (see instructions) |

11 |

|

|

|

|

|

|

b |

Other business property . . . |

20b |

|

|

|

|

||||||

12 |

Depletion |

12 |

|

|

|

|

|

|

21 |

Repairs and maintenance . . . |

21 |

|

|

|

|

||||||

13 |

Depreciation and section 179 |

|

|

|

|

|

|

|

22 |

Supplies (not included in Part III) . |

22 |

|

|

|

|

||||||

|

expense deduction |

(not |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

23 |

Taxes and licenses |

23 |

|

|

|

|

|||||||

|

included in Part III) (see |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

instructions) . . . . |

13 |

|

|

|

|

|

|

24 |

Travel and meals: |

|

|

|

|

|

|

|

||||

14 |

Employee benefit programs |

|

|

|

|

|

|

|

a |

Travel |

24a |

|

|

|

|

||||||

|

(other than on line 19) |

. |

14 |

|

|

|

|

|

|

b |

Deductible meals (see |

|

|

|

|

|

|

|

|||

15 |

Insurance (other than health) |

15 |

|

|

|

|

|

|

|

instructions) |

24b |

|

|

|

|

||||||

16 |

Interest (see instructions): |

|

|

|

|

|

|

|

25 |

Utilities |

25 |

|

|

|

|

||||||

a |

Mortgage (paid to banks, etc.) |

16a |

|

|

|

|

|

|

26 |

Wages (less employment credits) |

26 |

|

|

|

|

||||||

b |

Other |

16b |

|

|

|

|

|

|

27a |

Other expenses (from line 48) . . |

27a |

|

|

|

|

||||||

17 |

Legal and professional services |

17 |

|

|

|

|

|

|

b |

Reserved for future use . . . |

27b |

|

|

|

|

||||||

28 |

Total expenses before expenses for business use of home. Add lines 8 through 27a |

. ▶ |

28 |

|

|

|

|

||||||||||||||

29 |

Tentative profit or (loss). Subtract line 28 from line 7 |

29 |

|

|

|

|

|||||||||||||||

30 |

Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 |

|

|

|

|

|

|||||||||||||||

|

unless using the simplified method. See instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Simplified method filers only: Enter the total square footage of (a) your home: |

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

and (b) the part of your home used for business: |

|

|

|

|

|

|

|

. Use the Simplified |

|

|

|

|

|

|||||||

|

Method Worksheet in the instructions to figure the amount to enter on line 30 |

30 |

|

|

|

|

|||||||||||||||

31 |

Net profit or (loss). Subtract line 30 from line 29. |

|

|

|

|

|

|

|

} |

|

|

|

|

|

|

||||||

|

• If a profit, enter on both Schedule 1 (Form 1040), line 3, and on Schedule SE, line 2. (If you |

|

|

|

|

|

|

||||||||||||||

|

checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3. |

|

31 |

|

|

|

|

||||||||||||||

|

• If a loss, you must go to line 32. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

32 |

If you have a loss, check the box that describes your investment in this activity. See instructions. |

} |

|

|

|

|

|

|

|||||||||||||

|

• If you checked 32a, enter the loss on both Schedule 1 (Form 1040), line 3, and on Schedule |

|

|

|

|

|

|

||||||||||||||

|

SE, line 2. (If you checked the box on line 1, see the line 31 instructions.) Estates and trusts, enter on |

|

32a |

All investment is at risk. |

|||||||||||||||||

|

Form 1041, line 3. |

|

|

|

|

|

|

|

|

|

|

|

|

|

32b |

Some investment is not |

|||||

|

• If you checked 32b, you must attach Form 6198. Your loss may be limited. |

|

|

|

at risk. |

|

|

||||||||||||||

For Paperwork Reduction Act Notice, see the separate instructions. |

|

|

Cat. No. 11334P |

|

|

|

Schedule C (Form 1040) 2021 |

||||||||||||||

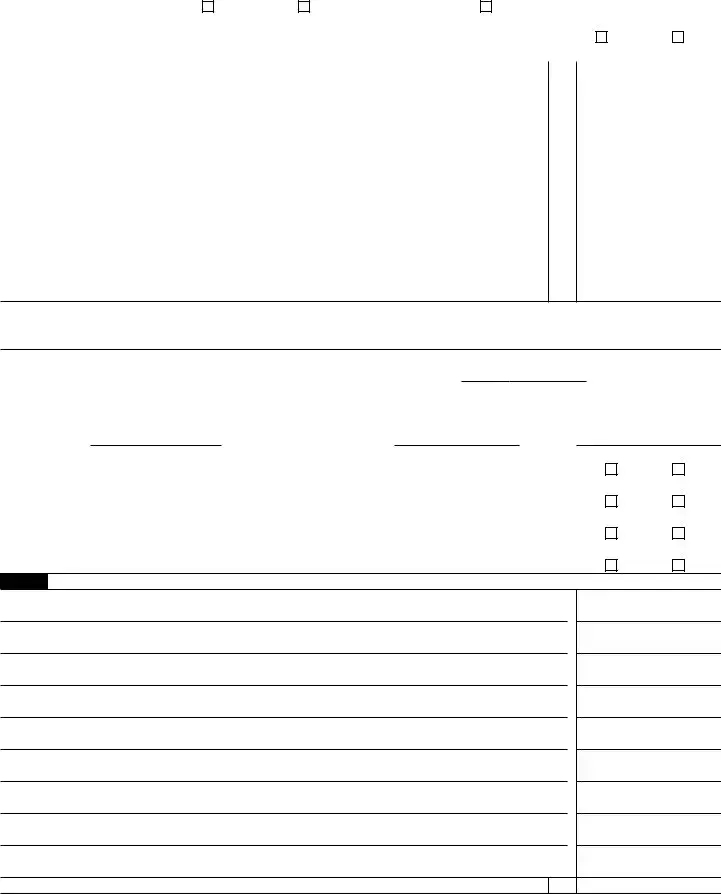

Schedule C (Form 1040) 2021 |

Page 2 |

|

Part III |

Cost of Goods Sold (see instructions) |

|

33 |

Method(s) used to |

|

|

|

|

|

|

|

value closing inventory: |

a |

Cost |

b |

Lower of cost or market |

c |

Other (attach explanation) |

34Was there any change in determining quantities, costs, or valuations between opening and closing inventory?

If “Yes,” attach explanation |

Yes |

No

35 |

Inventory at beginning of year. If different from last year’s closing inventory, attach explanation . . . |

35 |

36 |

Purchases less cost of items withdrawn for personal use |

36 |

37 |

Cost of labor. Do not include any amounts paid to yourself |

37 |

38 |

Materials and supplies |

38 |

39 |

Other costs |

39 |

40 |

Add lines 35 through 39 |

40 |

41 |

Inventory at end of year |

41 |

42 |

Cost of goods sold. Subtract line 41 from line 40. Enter the result here and on line 4 |

42 |

Part IV Information on Your Vehicle. Complete this part only if you are claiming car or truck expenses on line 9 and are not required to file Form 4562 for this business. See the instructions for line 13 to find out if you must file Form 4562.

43 |

When did you place your vehicle in service for business purposes? (month/day/year) |

▶ |

/ |

/ |

44Of the total number of miles you drove your vehicle during 2021, enter the number of miles you used your vehicle for:

a |

Business |

b Commuting (see instructions) |

c Other |

45 |

Was your vehicle available for personal use during |

||

46 |

Do you (or your spouse) have another vehicle available for personal use? |

||

47a |

Do you have evidence to support your deduction? |

||

b |

If “Yes,” is the evidence written? |

||

Yes

Yes

Yes

Yes

No

No

No

No

Part V Other Expenses. List below business expenses not included on lines

48 |

Total other expenses. Enter here and on line 27a |

48

Schedule C (Form 1040) 2021

Consider More Forms

Printable Direct Deposit Form - Be mindful that incomplete forms may lead to delays in setting up direct deposit.

When considering the sale of a recreational vehicle, understanding the importance of an Arizona RV Bill of Sale is crucial. This document ensures a smooth transaction, providing both parties with necessary proof of the sale. For more information about this process, refer to our guidelines on the important RV Bill of Sale requirements.

Free Printable Shower Sheets for Cna - It aids in developing best practices for skin monitoring among staff.